YNAB vs EveryDollar – Intro

In the ever-evolving landscape of personal finance management, choosing the right budgeting tool is crucial for achieving financial goals and maintaining a healthy financial life. Two prominent contenders in the market, YNAB (You Need A Budget) and EveryDollar, offer users robust solutions for budgeting and financial planning. In this comprehensive comparison, we’ll delve into the features, personal experiences, pricing structures, pros and cons, and explore alternative options before arriving at a verdict.

Content

Quick Comparison

For those seeking a swift answer, the choice between YNAB and EveryDollar ultimately depends on personal preferences and specific financial needs. YNAB excels in its emphasis on zero-based budgeting and real-time synchronization, while EveryDollar offers simplicity and ease of use. Now, let’s explore the nuances that make each of these tools unique.

Features

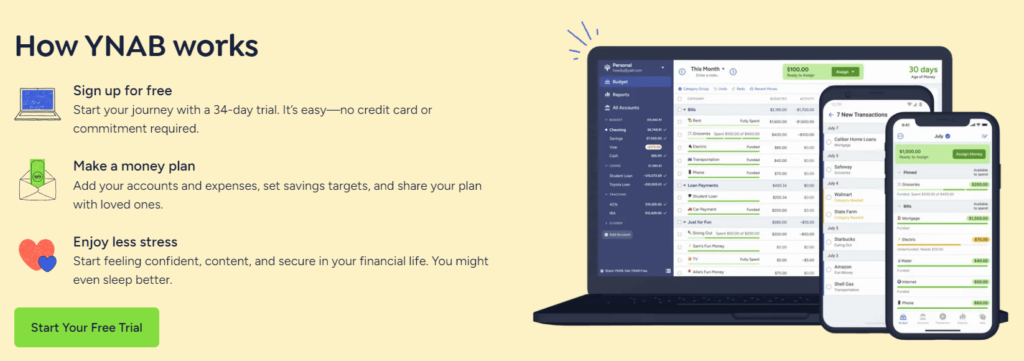

YNAB Features

YNAB is renowned for its commitment to the philosophy of zero-based budgeting. The platform provides users with real-time insights into their financial situation, encouraging intentional spending and helping break the paycheck-to-paycheck cycle. YNAB’s proactive approach to budgeting and robust goal-setting features are key highlights.

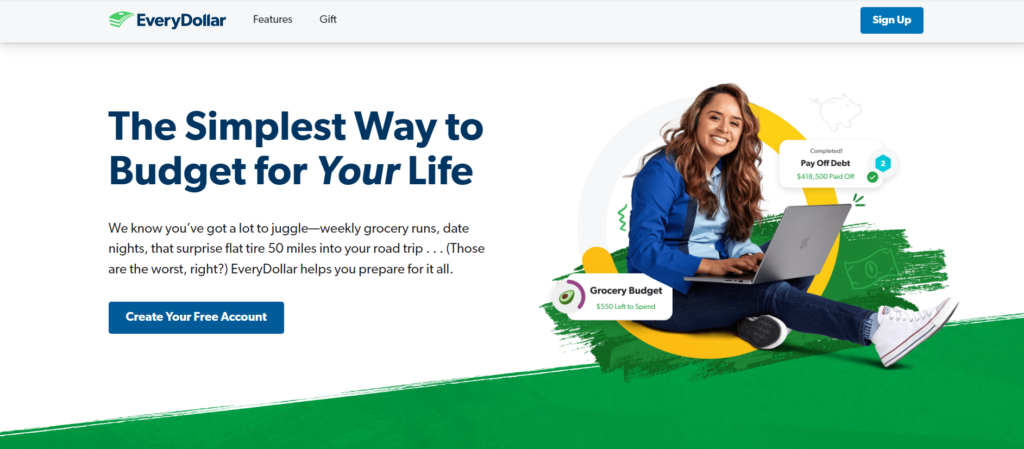

EveryDollar Features

EveryDollar, developed by financial expert Dave Ramsey, focuses on simplicity. The tool employs the zero-based budgeting approach but stands out with its user-friendly interface. EveryDollar’s strength lies in its straightforward budget creation, making it accessible for users who may be new to budgeting.

Personal Experience

Personal finance tools are inherently subjective, as users have unique preferences and financial situations. In my experience, YNAB provided a more immersive and detailed approach to budgeting. The emphasis on assigning every dollar a job and the ability to adjust budgets in real-time offered a level of control that resonated with my financial goals.

On the flip side, EveryDollar’s simplicity appealed to those who prefer a streamlined budgeting process. The straightforward layout and ease of use make it an excellent choice for individuals who are just beginning their financial journey.

Pricing

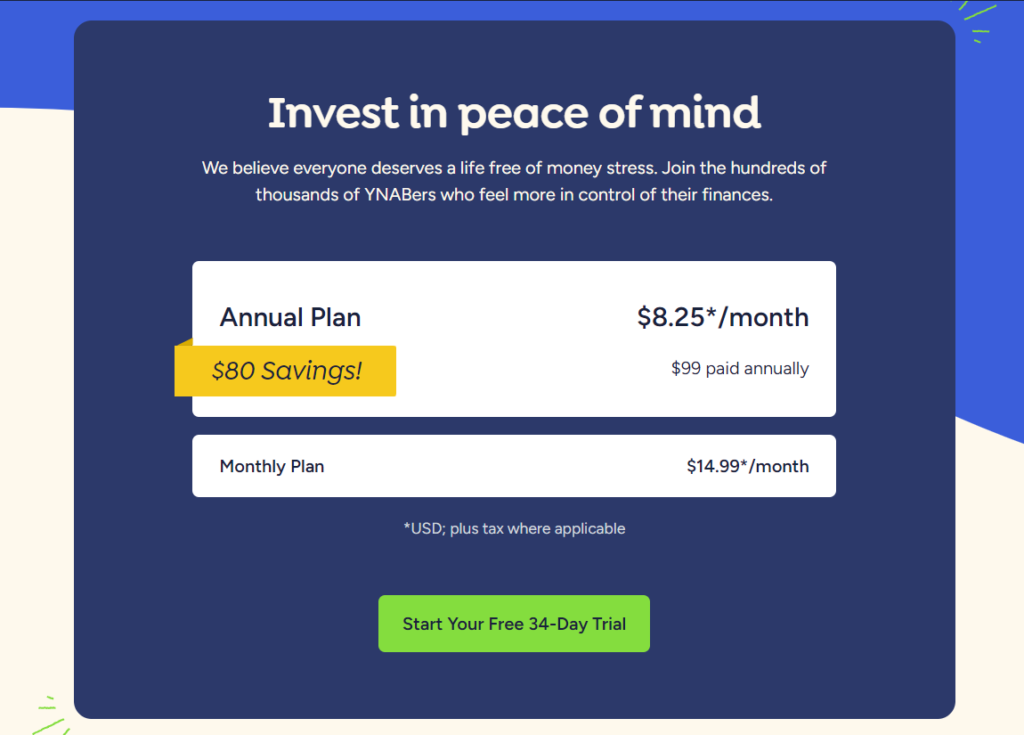

YNAB Pricing

YNAB operates on a subscription model with a monthly or annual fee. While the cost may seem prohibitive to some, many users find the investment worthwhile due to the tool’s comprehensive budgeting features and continuous updates.

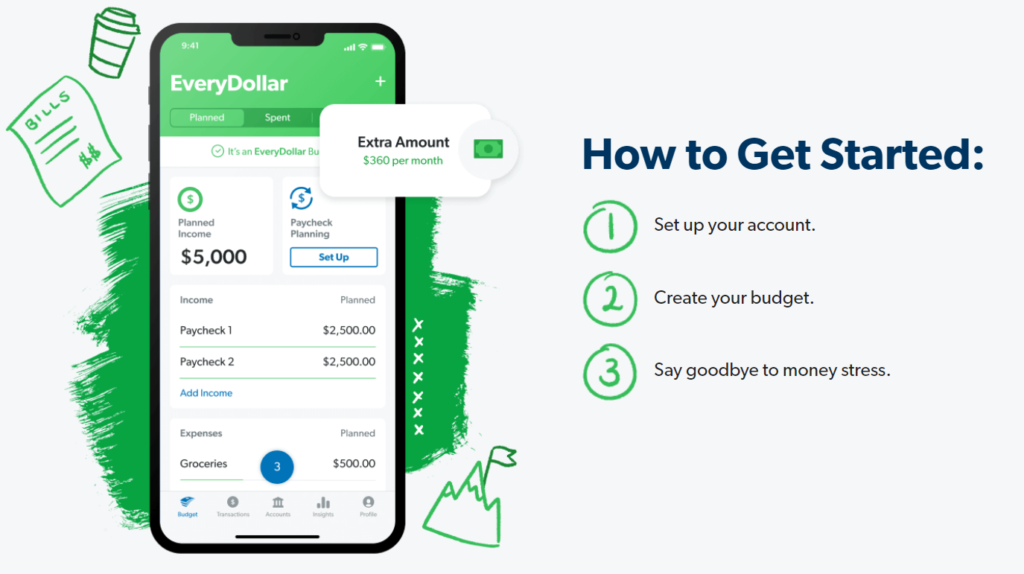

EveryDollar Pricing

EveryDollar offers a free version with limited functionality and a premium version at a monthly or annual subscription cost. The premium version unlocks additional features, including automatic transaction importing, which enhances the overall user experience.

YNAB vs EveryDollar – Pros & Cons

YNAB Pros & Cons

Pros:

- Zero-based budgeting philosophy.

- Real-time synchronization.

- Robust goal-setting features.

Cons:

- Monthly subscription cost may be a deterrent for some users.

EveryDollar Pros & Cons

Pros:

- User-friendly interface.

- Simplicity in budget creation.

- Developed by financial expert Dave Ramsey.

Cons:

- Free version has limited functionality.

- Automatic transaction importing is a premium feature.

Alternatives

In the realm of budgeting tools, alternatives to YNAB and EveryDollar include Mint, PocketSmith, and EveryDollar Plus. Each alternative caters to different preferences, so exploring these options is essential to finding the best fit for individual needs.

Conclusion/Summary: Who is the Winner?

After a thorough exploration of features, personal experiences, pricing, and pros and cons, the choice between YNAB and EveryDollar boils down to individual preferences and financial objectives. YNAB shines for those seeking a comprehensive and dynamic budgeting tool, while EveryDollar caters to users who prioritize simplicity and a straightforward approach.

In conclusion, the “best” budgeting tool depends on the user’s comfort level, financial goals, and willingness to invest in a subscription service. Ultimately, the winner is subjective and hinges on the unique needs of each individual or household. Before making a decision, it’s advisable to explore free trials, compare features, and consider personal preferences to determine which tool aligns best with specific financial aspirations.